Notes From JPM

NFTBC favourites BRKR and REGN both presented at the JPM Morgan Healthcare Conference

Friends of NFTBC

Both Bruker and Regeneron presented yesterday at JPM. I have combined some thoughts and notes into the same post. These are, of course, very different businesses except perhaps for their commitment to leading-edge science which serves as something of a commonality - that and unorthodox owner-operators at the helm. The plan here is to highlight anything I think is new or interesting, or where there’s an increase in the signal strength.

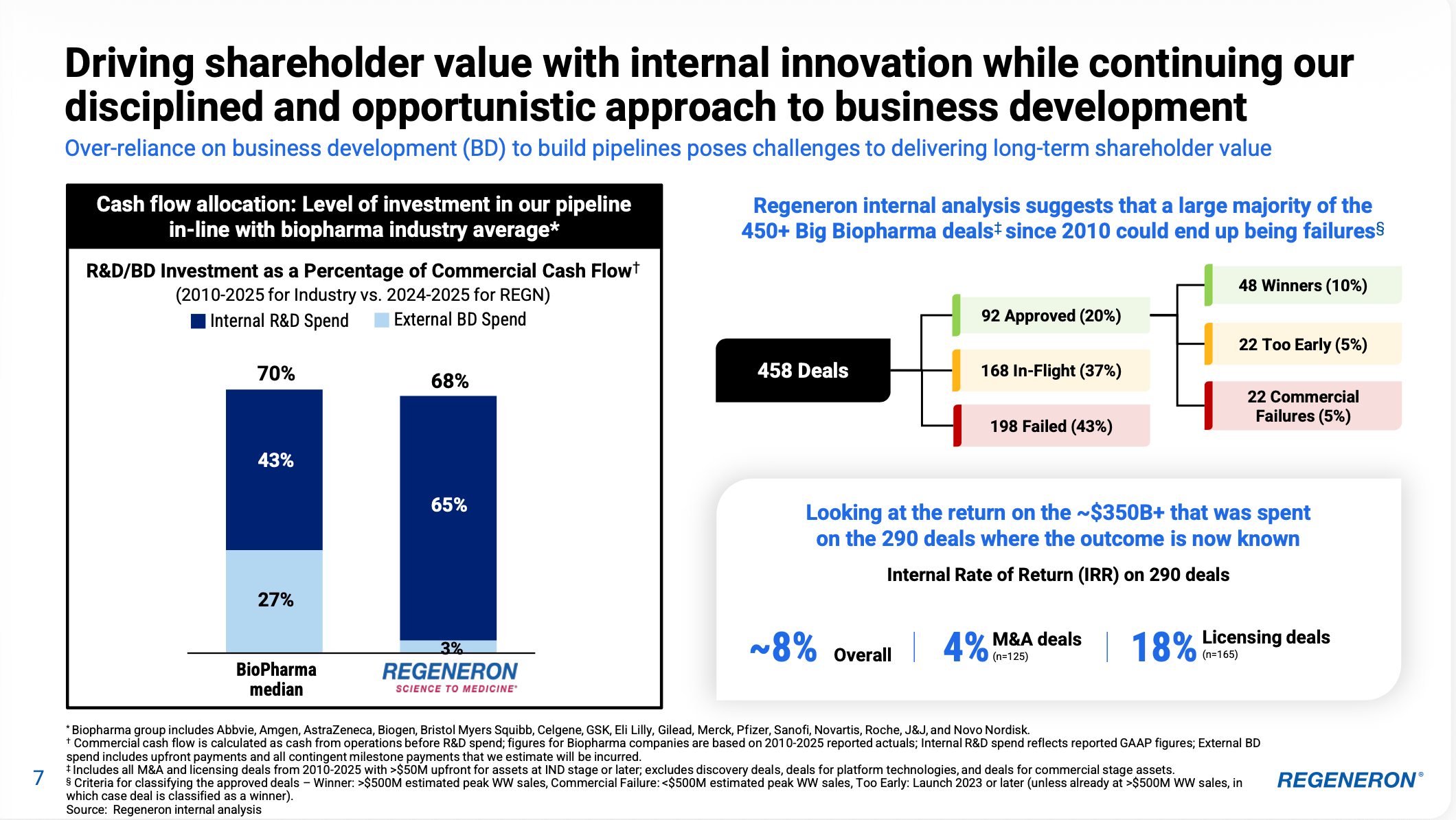

You can usually rely on Regeneron to come out with something at least a little unconventional at JPM. This year it was a slide, having a bit of a dig at industry practice:

As to the perennial question of whether or not Regeneron will finally do a major deal with its big cash pile, I suspect we have our answer. With that, let’s get going.

Bruker

BRKR put out an 8K yesterday and a slide deck.

Financials / outlook

Preliminary Q4 25 revenue USD 965m - 970m, implying full-year revenue USD 3.43bn +2% (flat in constant currency). This is marginally above consensus

Book-to-book still >1x

FY26 outlook (guidance in February): Flat to LSD organic revenue growth + 250-300bps operating margin expansion

And then very strong commitment beyond just ‘26 and taking a big step and a big swing in ‘26. For ‘27 through ‘30 really to deliver continued major margin expansion that may be 150 or 200 bps per year each year, hopefully, and double-digit non-GAAP EPS CAGR, while presumably by ‘27 returning to what we think our portfolio and should enable us to do, which is to deliver meaningfully above market revenue, organic revenue CAGR.

Thinking through the implications, Frank seems to be suggesting 900-1000bps margin expansion by 2030, which is roughly where I was thinking, if a bit ahead. He stopped short of providing a concrete target but suggested there would be an Investor Day later in the year.

A few early indicators on the 2026 outlook:

Not expecting a “snapback to our traditional growth rates right away”

“We had said we would aim for $100 million to $120 million of cost reductions, both COGS and OpEx, and we are very much we are very much focused on the high end of that. So we’re aiming to deliver $120 million of anticipated cost savings in 2026”

New BEST agreements: “that’s a big deal and removes a drag or a headwind to growth that was meaningful last year and that should reverse in ‘26 and beyond as well”

“we do have some early signs for sure on the mix side of the business that we will do better from a gross margin perspective in a number of our businesses”

Project Accelerate 3.0

It’s been a few years since they’ve added a new iteration of Project Accelerate, which Frank says is now at 60% of the business. It’s clear they’ve been heading in this direction anyway, but perhaps the drive for recurring revenue has now stepped up a gear:

Sometimes at Bruker, we say we work too hard for all the revenue. We have to deliver so much innovation, and that’s great. But last year, people weren’t quite as willing to work or to pay for innovation, for research instruments and ACA/GOV. So we’re very deliberately emphasizing more sticky, more aftermarket, more consumables business, more service businesses.