WPP Update

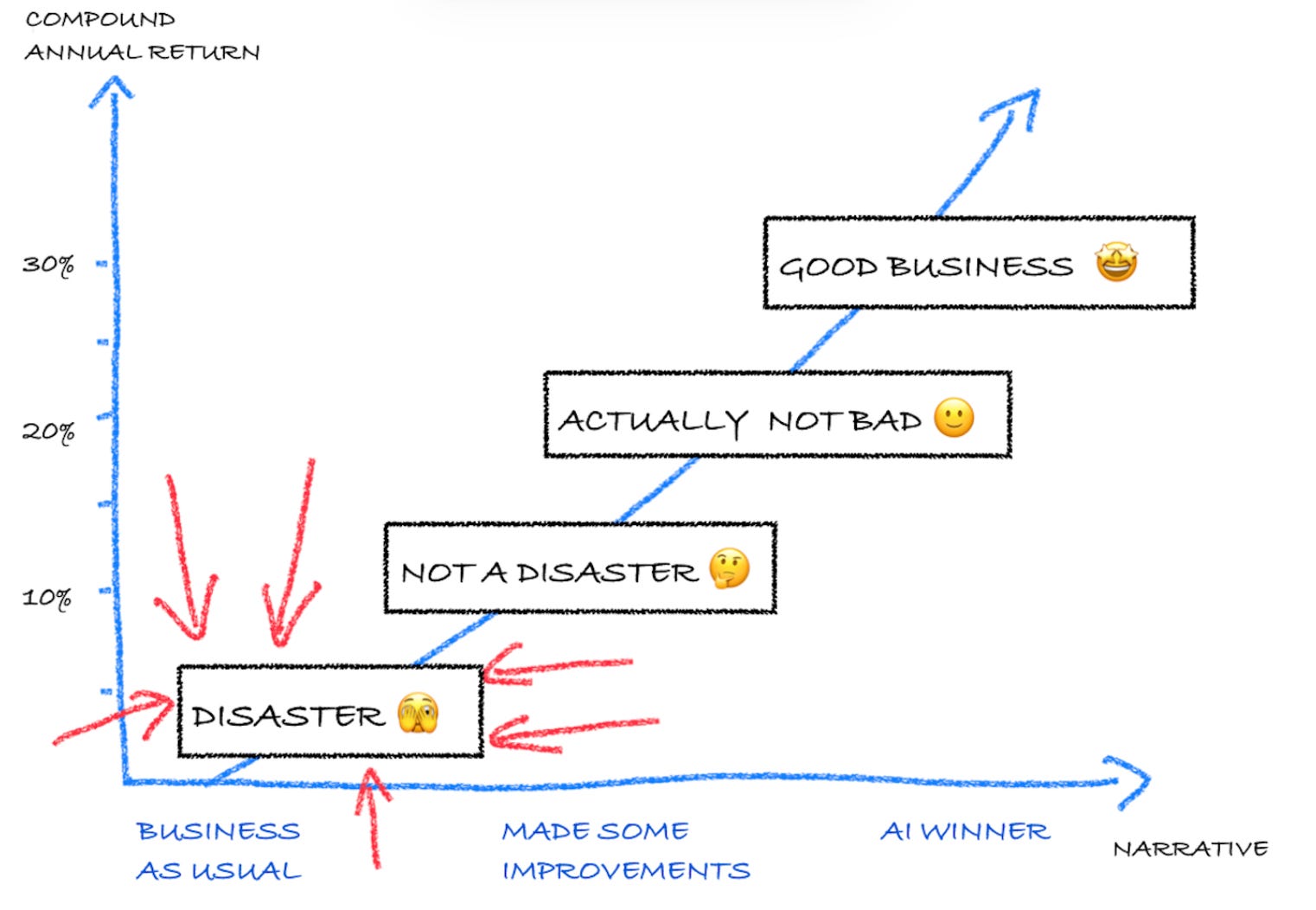

Disaster?

“I think I have, yes, and I think I can probably repeat them almost perfectly. I know my mistakes inside out.”

-Sir Arthur Streeb-Greebling, when asked if he had learnt from his mistakes

One of my many pitfalls as an investor is that of arriving too early - being well aware of it, I have made a few modifications to my process over the years to try to mitigate the effects. But it’s probably a bias I’m stuck with given my temperamental leaning towards getting into an opportunity before it’s obvious - I just prefer things that way. Along with a higher-than-average tolerance for looking foolish, it’s a potent combination.

It looks like I was too early to WPP - as evidenced by the precipitous 16% plunge in the shares following the company’s earnings update (welcome to the beauty contest!). As things stand, it’s not the end of the world - on a portfolio-weighted basis of my first two NFTBC ideas (REGN and WPP) they’re about flat since going live, which is around 3 percentage points better than the global index.

Let’s talk about what happened then.

[This is not intended as advice - please do your own research].

Along with its 2024 earnings today, WPP provided guidance for 2025. For all the reasons I outlined previously, I was expecting WPP to guide for an improvement in performance in 2025 - the signals seemed pretty strong. I thought it would probably be a fairly modest improvement, a partial bridge towards the medium-term targets - perhaps 1.5 to 2% organic revenue growth and another 20-40bps increase in operating margin. But what we were told was organic revenue growth of 0 to -2% and flat margin - roughly the same revenue performance as last year but with no margin improvement this time. If anything, a step backwards!

Given that Mark Read was still talking in January about doing better this year than last year, his credibility has certainly taken a knock. There are plausible explanations though - on the conference call today, it became clear that CFO Joanne Wilson was being intentionally cautious with the guidance. While, for his part, Read said they were “gunning for the top end”. Maybe he wanted to set a higher guide, but Wilson preferred caution. Who knows, but presumably back in January they hadn’t yet gone through the process of producing the guidance and perhaps he really did think they’d do better. We’ve also had the President of the United States saying all manner of things about tariffs in the last month since Read spoke to the FT - it wouldn’t be surprising at all to see how this could impact clients’ media plans and WPP does rather a lot of discretionary and project-based business. The ‘macro’ was specifically raised as one of the main considerations.

Regarding margins, we already knew that they were going to incrementally increase investment in technology again this year. But I hadn’t assumed this to be at the expense of their margin ambitions. I should have. Were it not for the increased investment, margins would go up this year - probably by a similar amount to last year. According to management, they’re seeing so much resonance with clients on WPP Open, they decided to make the investment because they believe it will drive growth and they’re maintaining their medium-term targets as a result - sounds great in principal, but they have to deliver now.

It looks like the first quarter of this year is going to be a rather slow one, with some remaining hangover from the headwinds I have discussed previously. And then from Q2 we have been told to expect those headwinds to abate and for last year’s new business wins to start ramping. I’ll be watching the ramp closely. Additionally, if Mark Read is going to earn back his credibility, I think WPP needs to demonstrate that it can maintain the new business momentum that we saw in the latter part of 2024. The more net new business they win, the more confident we can be. So those are the principal things I’ll be looking for.

For now I don’t intend to make any changes to my holding. I think it’s too early to conclude I was wrong, and things could turn quite quickly if the ramp and new business momentum are sufficiently strong. It’s clearly too early to tell if I’m right too, so I won’t be adding despite the cheaper share price. That said, if I didn’t already own the shares, I probably would buy some now.

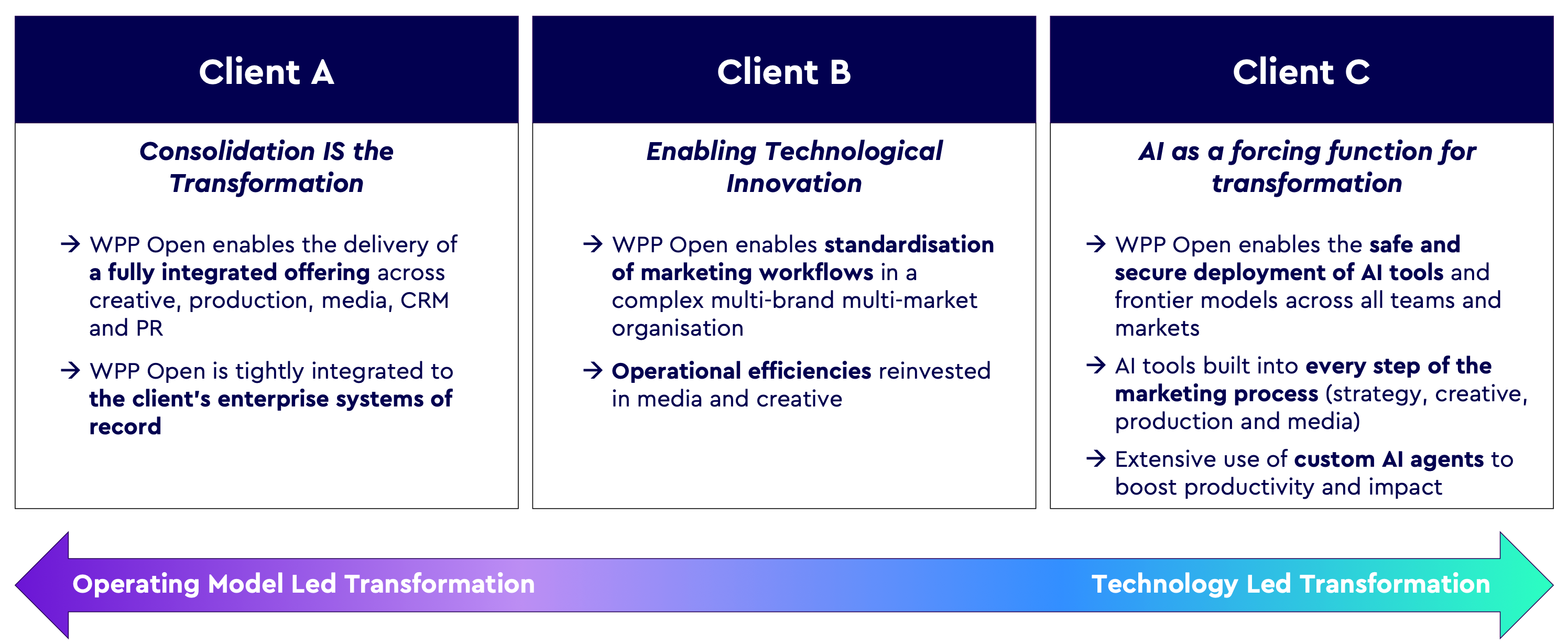

With all that out of the way, there were some genuinely exciting things discussed on the call that further strengthen the soundness of the WPP Open strategy - assuming they can execute. First of all, this:

One of the things I talked about previously was how WPP Open would likely lead to lower client churn, and WPP more or less validated today that they believe the same. Look at Client A - tight integration into the client’s ERP system sounds like an incredible way to build retention. ERP is about the stickiest thing there is. In Client B they talked about establishing themselves in client workflows - also sticky. While in Client C they specifically referenced the formation of a “sticky” relationship through technology services. One can’t really overstate the importance of lowering client churn while also becoming more important to the client.

There was an interesting discussion with the new head of GroupM too (WPP’s media business), and their strategy of moving clients away from legacy ID data strategies (i.e. that Publicis has been getting a lot of traction with) towards integration of disparate datasets through machine intelligence. Their ambition is for GroupM to be growing significantly faster.

I continue to believe the strategy to be a fundamentally sound and we’ve seen signals that it’s working - the success of the Coca-Cola account as well as major new client wins last year. But we do need to see WPP start to show further strong signs of progress this year. I previously said this would be a multi-year story, so we can afford to be a little bit patient. Patience, does however have its limits.

"Being too far ahead of your time is indistinguishable from being wrong”

-Howard Marks